The maritime extension of the EU Emissions Trading System, in force since 2024, introduces shipping into the EU’s cap-and-trade carbon market as part of the Fit for 55 package. Unlike efficiency-based frameworks such as CII or EEXI, EU ETS converts greenhouse gas emissions into a direct, monetised financial liability. It must therefore be treated as balance-sheet risk management rather than regulatory reporting alone — introducing market risk, operational risk, contractual risk, and liquidity risk simultaneously.

What Our Services Cover

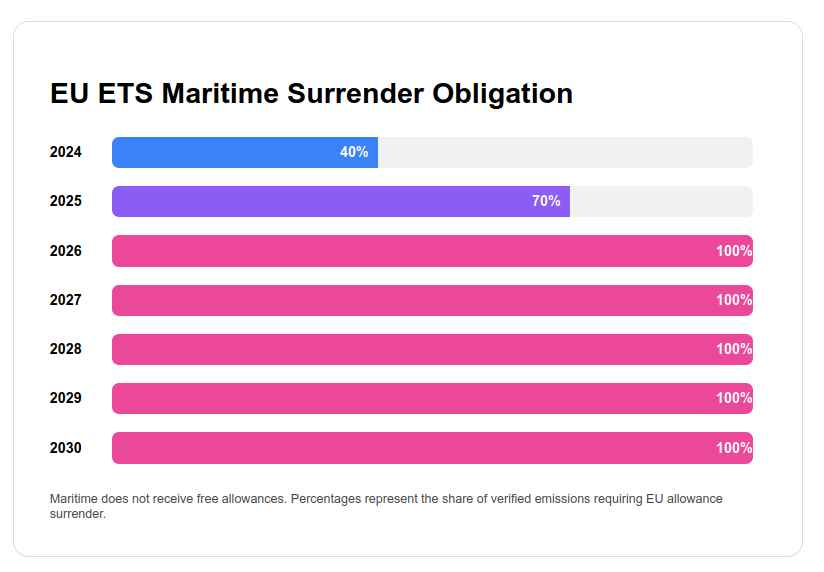

EU ETS applies to ships of 5,000 GT and above carrying cargo or passengers for commercial purposes. Coverage encompasses 100% of emissions from intra-EU voyages, 100% of emissions at berth in EU ports, and 50% of emissions on voyages between EU and non-EU ports. CO₂ is covered from 2024, with methane and nitrous oxide added from 2026, expanding financial exposure further. Surrender obligations are phased — 40% for 2024 emissions, 70% for 2025, and 100% from 2026 onward — but the phase-in merely staggers full liability rather than reducing it.

Our services begin with verified emissions quantification under the EU MRV Regulation, requiring careful segmentation of voyage data to distinguish intra-EU from extra-EU legs and allocate emissions accordingly. This verified baseline then forms the foundation for financial exposure modelling. Because EU allowance prices are subject to significant volatility — driven by macroeconomic conditions, policy developments, energy market dynamics, and speculative activity — our analysis incorporates low, base, and high carbon price scenarios across a forward horizon rather than assuming a fixed value. Each scenario is applied to projected emission volumes to estimate annual allowance procurement cost and its impact on operating margins.

Allowance procurement strategy is a core component of our services. We evaluate the cost implications of spot market purchasing, forward hedging, and inventory management under volatile price conditions, ensuring that procurement decisions are optimised for both cost and liquidity. We also model the annual cash flow cycle arising from the regulatory calendar — verified emissions reports due by 31 March and allowance surrender required by 30 September — to ensure liquidity planning is aligned with settlement obligations.

Our services extend to operational optimisation modelling, examining how fuel consumption patterns, vessel speed, port waiting times, and routing decisions affect absolute emissions and therefore allowance liability. Unlike CII, EU ETS is concerned with total emissions rather than intensity, meaning that operational decisions have a direct and quantifiable financial impact. These operational variables are assessed against commercial constraints, including charterparty obligations that may limit the flexibility available to reduce emissions through speed or routing adjustments.

Contractual exposure is another critical dimension. Legal responsibility under EU ETS rests with the shipping company as defined under the ISM Code, but the economic burden is frequently allocated between owners and charterers through charterparty EU ETS clauses. Poorly drafted or absent clauses can result in unexpected cost absorption. Our services include review and assessment of contractual exposure to ensure that cost allocation is clearly defined and commercially defensible.

Interaction with Other Regulatory Frameworks

In European waters, EU ETS overlaps with FuelEU Maritime greenhouse gas intensity requirements and, for applicable vessels, with SOx and NOx ECA obligations. From 2026, methane slip from LNG-fuelled vessels becomes directly relevant to EU ETS financial liability. Our services are structured to assess fuel pathway decisions across these overlapping regimes simultaneously, ensuring that compliance choices in one framework do not create unmanaged exposure in another.

Outputs and Deliverables

- Verified emissions baseline and voyage segmentation analysis

- Multi-scenario carbon price exposure modelling across a forward horizon

- Annual allowance procurement cost projections and cash flow planning

- Procurement strategy evaluation including hedging and inventory options

- Operational emissions reduction modelling and commercial constraint assessment

- Charterparty EU ETS clause review and contractual exposure assessment

- Capital expenditure sensitivity analysis incorporating carbon cost internalisation

- MRV monitoring plan review and data governance assessment

- Cross-regulatory interaction analysis covering FuelEU Maritime, ECAs, and CII

Strategic Value

EU ETS transforms carbon emissions from an environmental externality into a quantifiable and volatile operating expense embedded within a dynamic financial market. For vessels with structurally high fuel consumption or significant EU-linked trade exposure, the commercial implications are material and will intensify as surrender obligations reach 100% and the emissions cap continues to decline. Our services ensure that EU ETS exposure is actively managed — through emissions reduction, procurement optimisation, contractual clarity, and capital allocation — rather than passively absorbed as an uncontrolled cost.

What we do: We provide end-to-end EU ETS compliance and carbon exposure management for shipowners, operators, and managers.

A. Monitoring & Data Integrity

Monitoring Plan development and amendments

Fuel consumption validation

Voyage classification (intra-EU vs extra-EU)

GHG calculations in line with EU MRV methodology

B. Reporting & Registry Management

Annual emissions report preparation

Union Registry account setup and support

Documentation readiness for accredited verification bodies

C. Verification & Audit Readiness

Pre-verification compliance gap assessments

Technical liaison with accredited verifiers

Corrective action implementation

D. Carbon & Allowance Strategy

Emissions forecasting and exposure modelling

Budget impact analysis

Allowance procurement and timing strategy

Cost optimization aligned with fleet decarbonization plans

Strategic Considerations for Maritime Operators:

EU ETS compliance should not be treated as an isolated reporting exercise. It intersects with broader regulatory and commercial risks:

FuelEU Maritime (a separate regulation) introduces fuel intensity requirements and penalty exposure beginning 2025.

Carbon price volatility introduces balance sheet risk.

Charterparty clauses must allocate ETS cost responsibility clearly.

Decarbonization investments now have measurable carbon price payback implications.

Operators who integrate EU ETS compliance with fuel strategy, chartering structures, and fleet renewal planning will materially reduce long-term exposure.