The IMO’s Revised 2023 Greenhouse Gas Strategy represents the most consequential policy shift in maritime climate regulation to date. While not itself directly binding, it establishes the quantified ambition levels that will drive mandatory measures under MARPOL Annex VI through the coming decade and beyond. For shipowners and operators, the strategy is not a distant policy commitment — it is the framework within which capital allocation decisions being made today will either preserve or destroy fleet value by the 2040s.

The Regulatory Trajectory

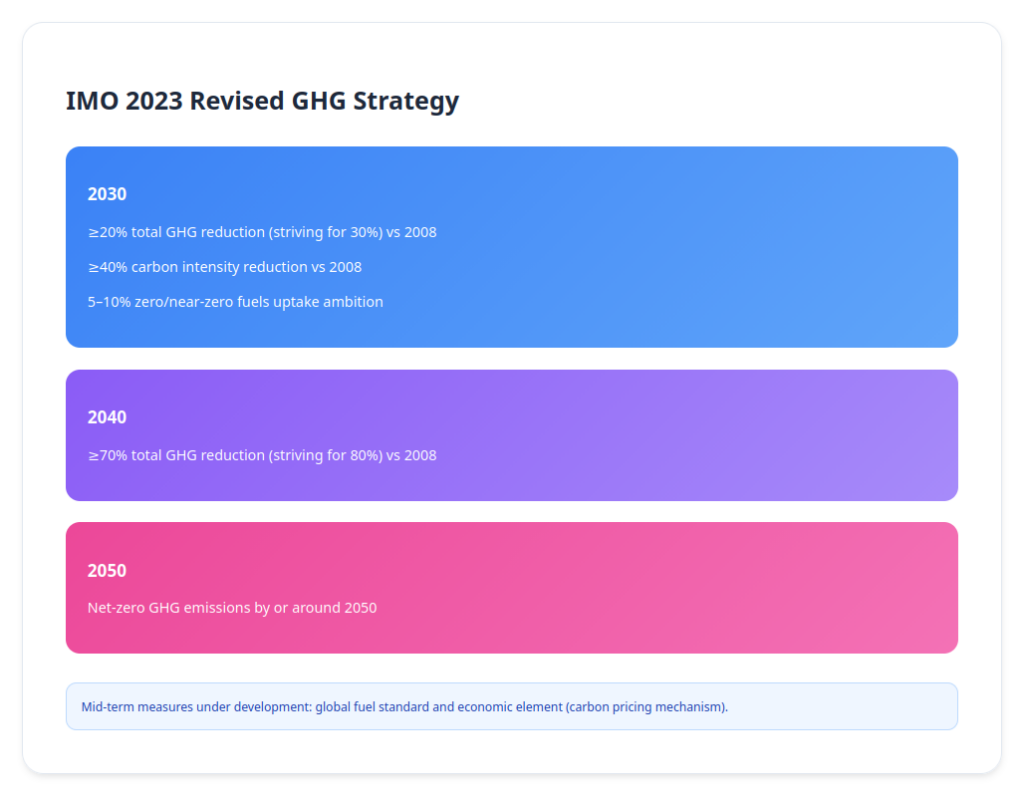

The strategy sets three principal ambition levels relative to 2008 emissions: a reduction of at least 20% in total annual GHG emissions by 2030 (striving for 30%), at least 70% by 2040 (striving for 80%), and net-zero by or around 2050. Alongside absolute emissions targets, the strategy maintains a carbon intensity ambition of at least 40% reduction by 2030, and establishes a target for zero- or near-zero emission fuels to represent at least 5% of shipping’s energy use by 2030. The distinction between absolute and intensity targets is critical: intensity improvements through efficiency measures alone will not deliver the systemic fuel transition that net-zero requires.

Translating strategy into obligation, IMO negotiations are currently focused on two binding mid-term instruments — a global greenhouse gas fuel standard and an economic mechanism, likely a carbon levy — expected to enter into force around 2027–2028. Lifecycle assessment guidelines are being finalised to establish well-to-wake emissions accounting, which will materially affect the regulatory and commercial treatment of fuels such as LNG, ammonia, methanol, and hydrogen. Our services track these developments continuously, providing clients with forward-looking assessment of how emerging mandatory measures will interact with existing regulatory obligations under CII, EEXI, EU ETS, and FuelEU Maritime.

What Our Services Cover

Our decarbonisation advisory services are structured around the recognition that no single fuel pathway currently dominates, and that the optimal strategy varies significantly by vessel type, trade route, asset age, and commercial structure. Our services provide rigorous, evidence-based evaluation of available pathways rather than advocacy for any particular technology or fuel.

Ammonia offers zero-carbon combustion and significant scale potential, but presents material toxicity risks, combustion complexity, and infrastructure constraints that must be carefully assessed before commitment. Methanol offers handling advantages and growing engine compatibility, but delivers genuine lifecycle decarbonisation only when produced from renewable feedstocks — a supply chain dependency that introduces its own commercial and contractual risks. Hydrogen presents zero-carbon combustion characteristics suited to fuel cell applications, particularly in shorter-sea trades, but faces storage, energy density, and infrastructure limitations that constrain near-term deep-sea scalability. Battery-electric and hybrid systems are effective in coastal and short-sea applications, particularly where shore power infrastructure is available, but energy density constraints limit their applicability for long-haul deployment. Each pathway is assessed under well-to-wake lifecycle emissions accounting, infrastructure availability, applicable safety regulations, and full capital cost implications across the vessel’s projected trading life.

Our services also address the structural challenge that the IMO targets cannot be met through incremental efficiency improvements alone. Conventional measures — hull optimisation, slow steaming, waste heat recovery — contribute to intensity reduction and remain valuable within the existing CII and EEXI frameworks, but are insufficient for deep absolute decarbonisation. Our advisory work is therefore structured to distinguish between near-term compliance optimisation and long-term fuel transition planning, ensuring that efficiency investments made today do not foreclose the retrofit optionality required for future regulatory environments.

A critical dimension of our services is asset-level transition risk assessment. Vessels ordered or acquired today may still be trading in 2050. Capital allocation decisions made between now and the mid-2030s will determine whether individual assets remain commercially viable in the regulatory environment that the IMO 2040 and 2050 ambitions will produce. Our services evaluate newbuild design specifications for dual-fuel capability and fuel flexibility, assess retrofit optionality for existing vessels, and identify assets that face accelerated obsolescence risk under plausible regulatory trajectories.

Interaction with Existing Regulatory Frameworks

The IMO GHG strategy does not replace existing obligations — it intensifies and extends them. Our services are structured to ensure that decarbonisation planning is integrated with compliance management across CII, EEXI, EU ETS, and FuelEU Maritime. Fuel transition decisions carry implications across all of these frameworks simultaneously, and a strategy optimised for one regulatory instrument may create unmanaged exposure under another. Well-to-wake lifecycle accounting, already central to FuelEU Maritime and the emerging IMO fuel standard, means that fuel supply chain decisions are now as consequential as onboard fuel consumption choices.

Outputs and Deliverables

- Regulatory trajectory assessment incorporating IMO mid-term measure developments and interaction with existing frameworks

- Vessel and fleet-level decarbonisation pathway analysis across ammonia, methanol, hydrogen, biofuel, and hybrid options

- Well-to-wake lifecycle emissions assessment for candidate fuel pathways

- Asset transition risk evaluation and obsolescence risk profiling

- Newbuild specification review for fuel flexibility and retrofit optionality

- Charterparty carbon allocation clause assessment and commercial structure advisory

- Green financing readiness assessment and documentation support

- Integrated near-term compliance and long-term transition roadmap

Strategic Value

The 2023 IMO Strategy transforms decarbonisation from a long-term aspiration into a medium-term commercial imperative. Vessels with no credible pathway to zero-emission fuel compatibility face not only regulatory risk but declining charter competitiveness, restricted access to green financing, and accelerating asset value erosion. Our services provide the analytical foundation and strategic clarity needed to navigate fuel transition decisions with confidence — ensuring that capital committed today is positioned for viability in the regulatory and commercial environment of the 2040s, not merely the compliance requirements of the present.

What we do: We help shipping companies develop comprehensive decarbonization strategies:

A. Baseline Assessment

- Current emissions inventory

- Fleet carbon footprint analysis

- Regulatory exposure mapping

B. Pathway Analysis

- Technology options for your fleet

- Fuel transition roadmaps

- Cost-benefit analysis

C. Regulatory Preparation

- IMO strategy compliance planning

- MTMs impact assessment

- Horizon scanning for 2027+

D. Investment Strategy

- Newbuild vs. retrofit analysis

- Alternative fuel procurement

- Green financing options